A statistical indicator of the distribution of returns for a certain securities or market index is called volatility. Generally speaking, a security is riskier the higher its volatility. Standard deviation or variation between returns from the same securities or market index are frequently used to calculate volatility.

Large swings either way are frequently linked to volatility in the financial markets. For instance, a market is deemed volatile when it has consistent increases and decreases of more than one percent in the stock market. When pricing options contracts, the volatility of an asset is a crucial consideration.

KEY KNOWLEDGE

Volatility is a statistical measure of an asset's return dispersion; it shows how much an asset's values move around the mean price.

Standard deviations of returns, option pricing models, and beta coefficients are a few methods for quantifying volatility.

Because the price of volatile assets is predicted to be less predictable, they are sometimes seen as riskier than less volatile ones.

Historical volatility tracks price fluctuations over preset time periods, whereas implied volatility predicts future market volatility.

One significant factor in determining the price of options is volatility.

Understanding Volatility in Share Market

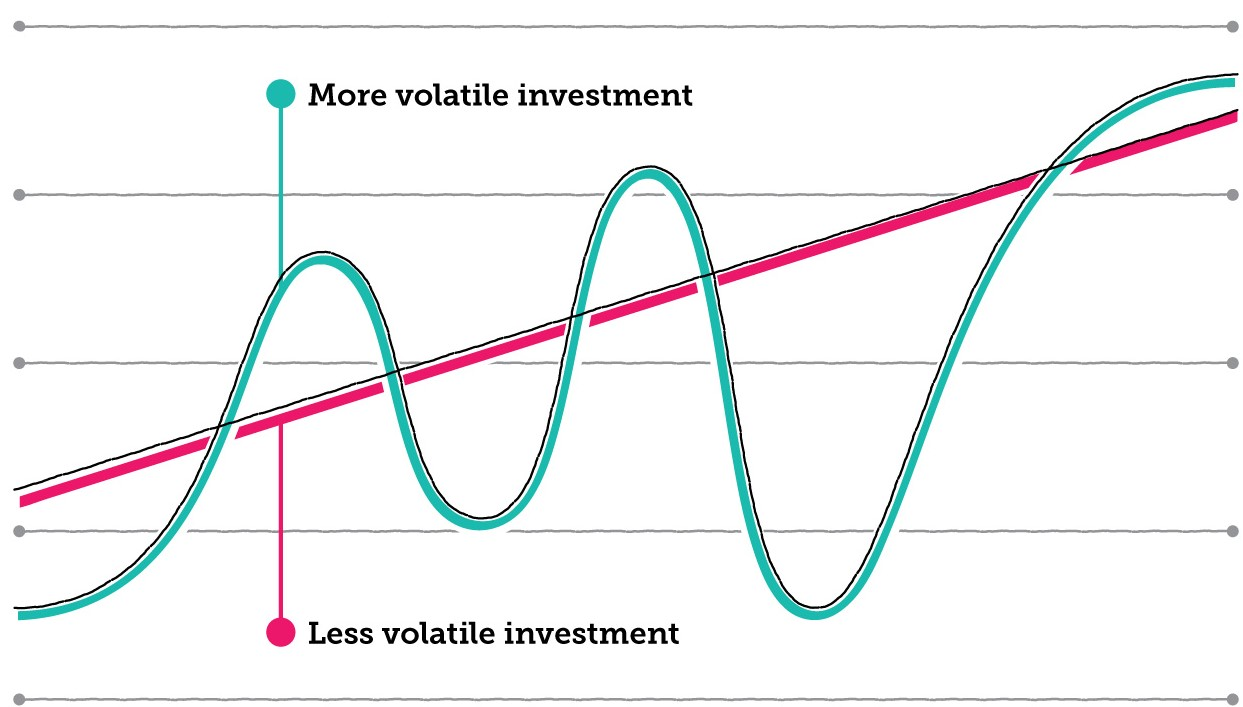

The degree of risk or uncertainty around the magnitude of fluctuations in a security's value is sometimes referred to as volatility. A higher volatility indicates the possibility of a wider range of values being covered by the value of the investment. This implies that the security's price may fluctuate significantly in either direction over a brief period of time. A lower volatility indicates that a security's value tends to be more stable and does not vary substantially.

Quantifying the daily returns (% change on a daily basis) of an asset is one technique to gauge its variety. Historical volatility, which is determined by past prices, is a measure of how variable an asset's returns can be. This figure is given as a percentage and lacks a unit.

Variance is a measure of an asset's overall return dispersion about its mean; on the other hand, volatility is same variance limited to a certain time interval. We may thus report volatility on a daily, weekly, monthly, or annually basis. Consequently, it is helpful to consider volatility to be the annualized standard deviation.

How to Calculate Volatility?

Variance and standard deviation are frequently used to calculate volatility (the standard deviation is the square root of the variance). Because volatility denotes variations across a certain time period, all you have to do is multiply the standard deviation by the square root of the number of periods in question:

vol = σ√T

Where:

V = volatility over some interval of time

σ = standard deviation in returns

T = Number of periods in the time horizon

Types of Volatility

Implied Volatility:

One of the most crucial indicators for options traders is implied volatility (IV), also referred to as predicted volatility. It does, as the name implies, enable them to estimate the degree of future market volatility. This idea also provides traders with a probability calculation method. It's crucial to remember that it shouldn't be regarded as science and, as such, cannot predict future market movements.

Inferred volatility, which is different from historical volatility, is derived from an option's actual price and indicates predictions for future volatility. Traders cannot use previous performance as a predictor of future performance since it is implied. Rather, they must make an assessment of the option's market potential.

Historical Volatility:

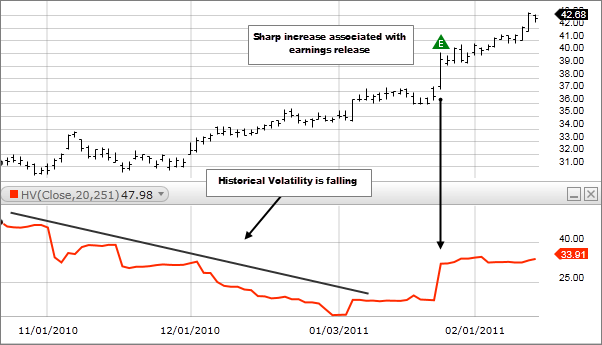

Historical volatility (HV), also known as statistical volatility, is a metric used to measure price movements over predefined periods of time in order to estimate the volatility of underlying assets. As it is not predictive, it is the less used statistic when compared to implied volatility.

The price of an asset will fluctuate more than usual when historical volatility rises. It is expected that something has changed, or will change, at this point. On the other hand, if historical volatility is declining, it indicates that all uncertainty has been removed and things have returned to normal.

Although this formula frequently evaluates fluctuations based on the shift from one closing price to the next, it may also be based on intraday variations. Historical volatility can be monitored in intervals of 10 to 180 trading days, depending on how long the options transaction is expected to last.

Volatility & Options Pricing:

In order to estimate how much the return of the underlying asset will change between now and the option's expiration, volatility is a crucial element in options pricing models. Daily trading activity are the source of volatility, which is represented as a percentage coefficient in option-pricing algorithms. The coefficient's value will vary depending on how volatility is quantified.

Models like Black-Scholes or binomial tree models price options contracts based on volatility as well. larger options premiums will result from more volatile underlying assets since there is a larger chance that the options will expire in the money when there is volatility. The price of an option in the market represents its implied volatility, which is determined by options traders attempting to forecast the future volatility of an asset.

IMPORTANT

The greater the volatility, the higher the market price of options contracts across the board.

Freqeuntly Asked Questions:

Political and economic factors

Monthly jobs reports, inflation data, consumer spending figures and quarterly GDP calculations can all impact market performance. In contrast, if these miss market expectations, markets may become more volatile.

In September 2019, JPMorgan Chase determined the effect of US President Donald Trump's tweets, and called it the Volfefe index combining volatility and the covfefe meme.

Volatility is the rate at which the price of a stock increases or decreases over a particular period. Higher stock price volatility often means higher risk and helps an investor to estimate the fluctuations that may happen in the future.

However, rather than increase linearly, the volatility increases with the square-root of time as time increases, because some fluctuations are expected to cancel each other out, so the most likely deviation after twice the time will not be twice the distance from zero.